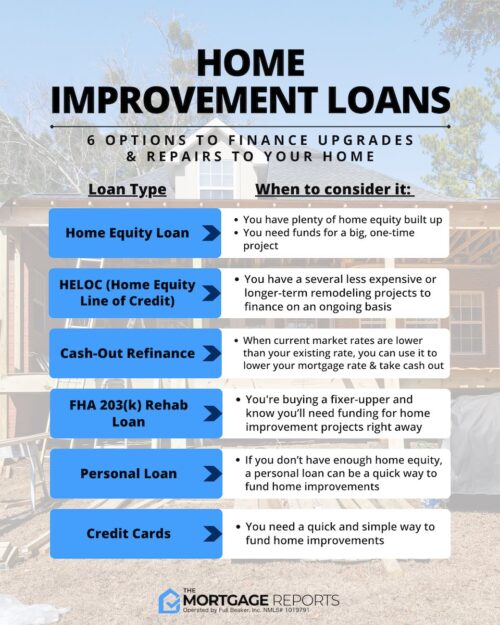

Most homeowners think they have to dig into their home equity to fund a major renovation. They assume the only way to pay for a new kitchen or a finished basement is through a second mortgage or a home equity line of credit. That’s a misunderstanding of how modern consumer credit actually works.

You don’t actually have to put your house on the line to fix your house. Relying only on equity can be a gamble. If the housing market takes a sudden downturn and you end up “underwater”—meaning your loan is bigger than your home’s value, you’re in a tough spot. Using your home as collateral for a project that might not immediately boost your property value is a high-stakes move that most people should avoid unless they have a very good reason.

Unsecured personal loans have changed the math. These loans don’t care about your home’s value; they care about your credit score and whether your income can cover the debt. That distinction is everything. With an unsecured loan, you aren’t handing over the deed to your home just to get a new roof.

Breaking Down the Unsecured Model

The biggest plus for an unsecured loan is speed. When you apply for a home equity loan, the bank wants an appraisal, a title search, and a mountain of paperwork. That takes weeks or even months. With a personal loan, you can often get an answer in hours and have the cash in your account within a few business days.

But speed comes with a price. You usually pay for that convenience through higher interest rates. Because the lender can’t seize your house if you stop paying, they take on more risk. That risk shows up in the APR. You have to weigh the convenience of fast cash against the long-term cost of the interest you’ll pay over the life of the loan.

I’ve seen people get caught in the middle because they don’t compare offers. They just take the first thing their local branch offers. That’s a mistake. You need to look at the total cost of the loan, not just the monthly payment. A lower monthly payment over a 72-month term might look good, but it will cost you thousands more in interest than a 36-month term.

Compare these common structures to see where you stand:

| Loan Type | Collateral Required | Approval Speed | Interest Rate Trend |

|---|---|---|---|

| Home Equity Loan | Yes (Your Home) | Slow (Weeks/Months) | Generally Lower |

| Personal Loan | No | Fast (Days) | Moderate to High |

| HELOC | Yes (Your Home) | Moderate | Variable (Changes) |

If you’re looking for significant capital for a total overhaul, you might need high-limit personal loans for major home renovations. These are designed for big projects, offering unsecured funding that can reach $100K or more. It’s a niche for people who want the scale of a mortgage-backed loan without risking their actual property title.

The flexibility is massive. Many people search for local options like texasloanstoday.com to understand what’s available in their area, but digital lenders have largely caught up. You can shop from your couch and get a decision before your coffee gets cold.

The Math Behind the Money

Interest rates are the most volatile part of this. You can’t walk into a bank and expect the same rate you saw on a billboard. Your debt-to-income ratio, your credit score, and your employment history dictate the terms. If your score is in the 700s, you’re in a much better position to get the lower end of the market rates.

For example, if you’re looking for specific benchmarks, unsecured home improvement personal loans from Wells Fargo can offer rates starting as low as 6.74%. That’s a competitive number, but remember, that’s the floor. Most people will land somewhere in the middle of the range.

Then there are origination fees. Some lenders charge a fee just to process the loan, and they often take it out of your principal before you see the money. If you borrow $10,000 and there’s a 5% origination fee, you only get $9,500, but you still owe interest on the full $10,000. It’s a sneaky way for lenders to pad their margins.

The good news is that not all lenders play that game. You can find cleaner options. For instance, you can get up to $40,000 with no origination fee, from Discover. Avoiding that upfront cost can save you a few hundred or even a thousand dollars depending on how much you borrow. It’s a small detail, but it matters when you’re trying to stay on budget.

Don’t forget the term length. U.S. Bank offers various options where you can choose a term from 12 months up to 84 months for certain products, though many personal loans cap out much earlier. A shorter term means a higher monthly payment but much less interest paid over time. You have to decide if your monthly cash flow can handle the squeeze.

Choosing Your Financing Strategy

Not every project is a kitchen remodel. Some people just need a new water heater or a repaired roof. If your needs are small, a personal loan might be overkill. You might be better off using a dedicated home improvement line of credit or even a high-yield savings account if you have the discipline to save up first.

But if you’re looking at a major aesthetic or structural change, the strategy shifts. You need to think about the ROI. A new bathroom might add $15,000 to your home’s value, but if the renovation costs $20,000, you haven’t really “won” in terms of equity. You’ve just traded liquid cash for a different kind of equity.

Credit unions often provide the best service. If you’re a military member or a veteran, Navy Federal is a major player here. They offer a wide variety of options, including home equity loans and other tools for renovations or emergency repairs. Their rates are often better because they are non-profit entities focused on their members.

- Emergency Repairs: Focus on speed and low origination fees.

- Cosmetic Upgrades: Focus on low monthly payments to manage cash flow.

- Major Renovations: Focus on high limits and total interest costs.

Avoid the “minimum payment” mindset. It works for credit cards, but it’s a slow death for a personal loan. If you take out a 60-month loan, try to pay it off in 36. Even an extra $50 a month can shave months off the end of your term and save you hundreds in interest. It’s the smartest move you can make.

The Hidden Costs of “Free” Money

People often overlook closing costs and prepayment penalties. Some loans are easy to get into but hard to get out of. If you decide to sell your house or refinance your mortgage next year, you don’t want a personal loan that charges a massive fee for paying it off early. It’s how banks ensure they get their interest regardless of what happens with your finances.

Also, check the fine print on variable vs. fixed rates. A fixed rate is better if you think interest rates will rise. A variable rate might look cheaper today, but it can become an expensive nightmare if the economy shifts. I’ve seen too many homeowners get blindsided by a sudden jump in their monthly obligations because they chased a lower initial rate.

Check your credit report before you start applying. A single error can push your interest rate up by a full percentage point. That sounds small, but over a five-year loan, it adds up to a lot of money. It’s worth the hour of work to pull your reports and make sure everything is accurate before you walk into the bank.

Sometimes, the best loan is the one you don’t need. If you can delay the renovation by six months and save the cash, you avoid the debt entirely. Debt is a tool, but it’s a sharp one. Use it with precision, or it will cut you when you least expect it.

The market won’t wait for you to be ready.

Questions people ask

Is a personal loan better than a home equity loan for home improvements?

Personal loans offer faster funding and easier approval without using your home as collateral, while home equity loans typically provide lower interest rates for larger projects.

Can I use a personal loan for home renovations?

Yes, most personal loans are unsecured and can be used for any legal purpose, including kitchen remodels, roofing, or landscaping.

How does a personal loan affect my credit score?

Applying for a loan involves a hard inquiry which may temporarily lower your score, but consistent on-time repayments can improve your credit history over time.

What are the typical interest rates for home improvement personal loans?

Interest rates vary based on your credit score and income, but they are generally fixed and range from low-interest rates for excellent credit to higher rates for fair credit.

Do I need to provide documentation for a personal loan?

Lenders typically require proof of income, such as recent pay stubs or tax returns, and identification to verify your ability to repay the loan.